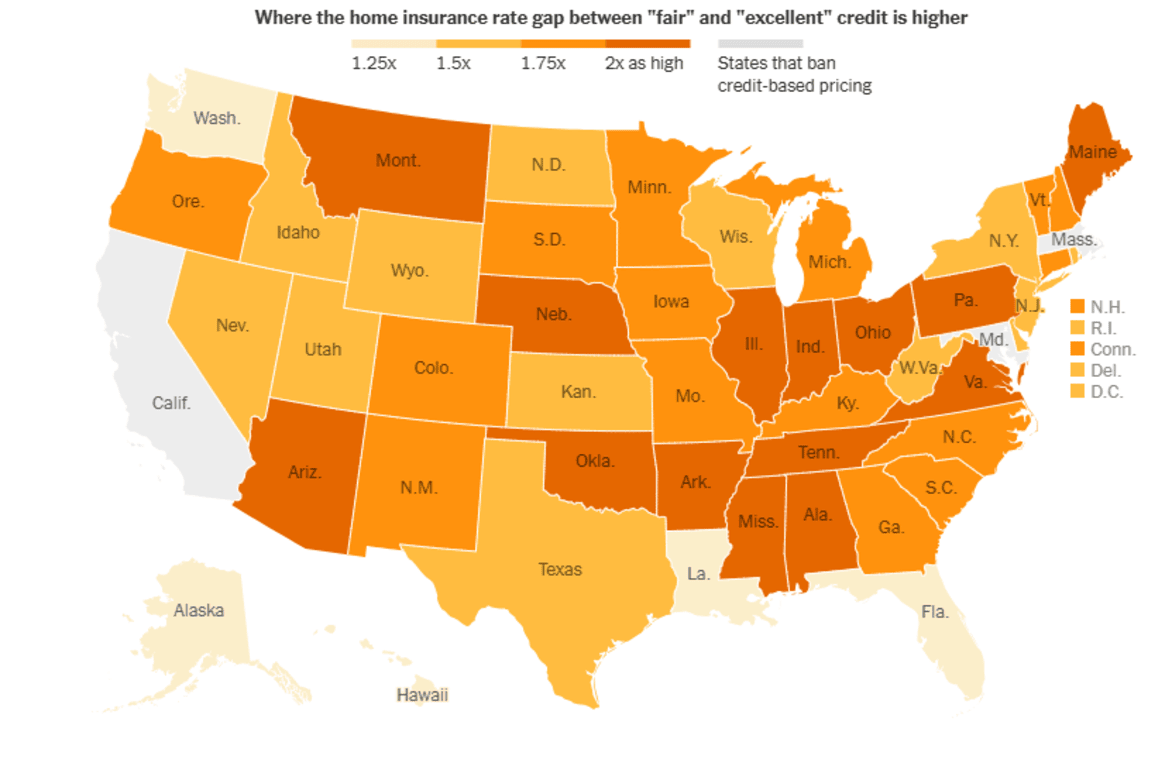

The New York Times has mapped how much more homeowners with weaker credit pay for home insurance compared to their homeowners with strong credit, state by state. The data comes from state regulatory filings—rate schedules insurers are legally required to submit. In darker states like Montana, Nebraska, and Arizona, the gap is largest, with weaker-credit homeowners paying double what people with strong credit pays for the same coverage. In lighter states the gap is smaller.

Visualizing the Credit Score Penalty in Home Insurance

previous post